Last week, I outlined three important rules that govern basic finances, and used those rules to justify why you need to invest. Those rules are:

- Make every dollar work for you.

- Inflation will erode the buying power of every dollar you save.

- Time is your best friend in fighting inflation, as it allows you to harness the power of compound interest.

The fact that you’ve come back to read part 2 of On the Origin of Investing, suggests I’ve successfully convinced you that you need to start saving for retirement, and start thinking about investing. Welcome to the party!

I’m sorry to say, however, that the last chapter may have been the easy part for both you and I. We had a bit of math to crunch (and that’s the foundation of everything we’re doing), but in order to invest, we actually need to understand the environment in which we are investing.

This will be the most dense chapter in this series, but it truly is essential to be familiar with this terminology if you’re going to be able to follow the final three parts in this series.

So… let’s do this!

The environment we are investing in is not your community. It is not your current circumstances. It is not even the economy. The environment we are investing in is the whole world, and everything that happens within it has an impact on what happens to the dollars we deploy.

We have to concern ourself with markets. Supply and demand. What do people want to buy and how can we make money off of it? Where do we find value? What kind of an impact is the new CEO going to have, or a new government, or the next big startup?

What is a stock market? What does it mean when I buy a stock? What’s a penny stock? What’s a blue chip stock? What else can I invest in?

I hope to answer all of these questions, and more, in the coming pages as we discuss The Stock Market, Equities, Fixed Income, and Funds.

The Stock Market(s)

The stock markets, and there are many, are a physical location where stocks are bought and sold (what’s a stock? see the next section).

The Toronto Stock Exchange (TSX), the New York Stock Exchange (NYSE), the London Stock Exchange (LSE), the Frankfurt Stock Exchange (FWB), and the Shanghai Stock Exchange (SSE). Each of these is a store, where stock brokers take orders to buy and sell shares in companies that are listed on that particular stock exchange.

For example, in the TSX, shares in Bell Canada (BCE-T) trade at volumes of over 1 million shares per day (they also sell on the NYSE at BCE-N). Shares in Apple Inc. are traded on the NYSE (AAPL-Q) at volumes of over 60 million shares per day.

By definition, these companies are publicly traded (as in, there is no one family or person who owns the company outright), and therefore can be purchased by anyone with the money to do so.

While understanding that these are simply the physical places where stocks are bought and sold (hence, a market), you may be more interested in traditional measures of the performance of these markets.

In order to understand how each of these markets is doing, we look at stock market indices.

Stock market indices track the overall performance of companies listed within the specific stock exchange. It’s the Cole’s Notes summary of how each company on the exchange did for the day, rather than having to read every single chapter (a report on each company). Some of these indices are more broad, while others narrow down to specific sectors of a country’s economy.

You may have heard of the S&P/TSX Composite Index, the TSX Venture, the S&P 500, the Dow Jones Industrial Average (DJIA), the Nikkei 225, the Hang Seng Index. What these indices try to capture is the overall strength of an economy, or at least, the value of the companies within that index.

For example, the S&P/TSX Composite Index, (S&P, by the way, is short for Standard & Poor’s), follows the price of the largest companies on the TSX, by market capitalization*, and represents approximately 70% of the total market capitalization of companies traded on the TSX. The S&P 500 represents the 500 largest companies being traded in the NYSE or the NASDAQ (another major American stock exchange).

*Also abbreviated as market cap, it indicates how much a company is worth, based on price, and multiplied by the number of shares the company has issued. A higher market cap means a company is worth more.

As a result, each index is essentially a snap shot of the day’s market activity.

Because indices are an easy way to communicate, in broad strokes, about the overall progress in the economy, you will often see these indices reported on your favourite news station during the financial segment. Now you’ll know what they’re talking about!

We’ll come back to indices later when we talk about funds.

Equities

Let’s cut to the chase. I keep talking about stocks, shares, equities. All of these mean essentially the same thing.

An equity (or a share, or a stock) is a fraction of a company’s worth that is sold on the stock market. By buying a share in the company, you are a shareholder, and are literally becoming a co-owner in the company (one of thousands, in most cases). Being a co-owner in a business comes with risk and reward.

The risks are obvious; if the company you own performs poorly, or goes out of business, then the value of your ownership takes a significant cut. The value may even be wiped out completely.

The benefits, however, are also tantalizing. As a co-owner, you are entitled to profits generated by the company. These profits may come in the form of dividend** payments, or they may come in the form of increased company valuation (which makes each share worth a little more, and therefore makes you some money).

**Dividends are monthly, quarterly, or yearly disbursements of CASH to shareholders of a company, and represent a portion of the profits generated by the company.

There are many factors that go into the valuation of a stock, but what is important to remember is that a stock is a commodity. It is subject to SUPPLY and DEMAND.

Therefore, if demand for a stock rises because a company is performing particularly well, the value of each stock increases to satisfy the demand.

If a company is doing poorly, the demand may go down, and the supply may go up (as shareholders may be eager to get off the sinking ship, and put their shares up for sale). These things in combination will cause the value of each stock to decrease.

The law of supply and demand is ultimately what dictates the value of a share, but what actually creates demand? What actually creates value?

Let’s start from the ground up, literally.

A company you own a share in is a living, breathing entity. It exists. As a result, there is tangible value in a company. This tangible value, at its simplest level, is how much money the company is worth without any business operations. The properties owned, the computers inside those properties, the heavy equipment, and factories. All of these things have concrete value because they are concrete things, and therefore make up a portion of the stock’s price. This portion is called the book value***.

***I’m sorry I have to do this, but book value has two meanings.

First, as above, the company’s tangible assets.

Second, in the realm of personal finance, the book value is how much an individual paid for a stock, or stocks (the price in your accounting book), which is helpful in determining the performance of your investments.

However, when we purchase a company, we aren’t only purchasing its assets, we are purchasing the work of the people employed, and the potential for growth in the company. In this, there is intangible value, because we can’t sell off our employees at the end of the day, and we can’t be sure how the company will grow.

Still, we appreciate talented engineers, convincing salespeople, and intelligent management, all of whom work towards growing the company. We’re willing to pay for these things because these things are what make the business run, and generate increasing profits. Therefore, we pay a little (or a lot) more for the stock based on what we think that business is worth. This is called market value, because the market decides what that intangible value is worth.

Market value and book value creates an important ratio in evaluating a company: it’s Price/Book (P/B) ratio. A low P/B ratio suggests that the price of a stock is well backed by its tangible assets. A higher P/B ratio suggests that the company’s stock price has more to do with the company’s intangible assets (like potential for profit growth, and creative management). A company with a low P/B ratio is not necessarily better or worse than a company with a high P/B ratio, but it is helpful to know what you are paying for.

Example: Fortis Inc (FTS), a utility company offers 250 million shares in it’s company at a value of $40 per share. This values the company at $10 billion dollars.

FTS generating stations, offices, and conduction equipment, versus their minor commercial debt has an estimated worth of $5 billion dollars.

This means that shares of FTS have a P/B ratio of 2.0 (10/5), and that investors believe the possibility for profit growth is high enough to justify a stock price twice that of its book value.

Another key ratio in understanding the position of a stock is its Price/Earnings (PE) ratio. Similarly to the P/B ratio, the PE ratio is calculated by dividing a share’s price by its annual earnings per share (EPS). It tells you how many dollars an investor is willing to pay for each dollar earned by the company. The reason that this is helpful is because it helps you to understand how highly valued a company is by investors. Given two companies with identical earnings, a higher PE ratio suggests that a company’s shares are highly valued because investors are willing to pay more for each dollar made, than a company with a lower PE ratio.

Example: Bank of Nova Scotia (BNS) and Bell Canada Enterprises Inc. (BCE) both have a share price of $50.

BNS earns $5 per share, giving BNS a PE ratio of 10 (50/5=10).

BCE earns $2.50 per share, giving BCE a PE ratio of 20 (50/2.50=20).

This means that investors are willing to pay twice as much for every dollar earned by BCE than they would for BNS, which may mean BCE is overvalued, or it may mean that investors see more potential for earnings growth in BCE, giving it higher value.

The difficulty with stocks, and you may be starting to recognize this, is that our investments are heavily tied to investor sentiment. Many people buy and sell on the stock market without really knowing why they are buying and selling. It may be a tip from a friend, or a news headline might scare investors about an impending sell off. We, as humans, are extremely emotional, especially when it comes to losing and gaining money (in the next chapter, we’ll talk more about the mindset necessary for successful investing).

What this means is that our investments can be wiped out when sentiment turns the wrong way. Of course, our investments can balloon if we get on early before investor sentiment becomes rosy. Stocks are inherently volatile as a result of emotional buying and selling. Owning stock is often likened to riding a roller coaster, but there are good ways and bad ways of riding a roller coaster, which we’ll talk about more in Chapter 5, on investment strategies.

Blue Chip Stock: a giant company with a solid reputation, usually with dependable earnings, often paying dividends.

Penny Stock: a common stock valued at less than $1 per share, therefore minor fluctuations in price have enormous impact on holdings; highly volatile and speculative.

Fixed Income (Securities)

What would Ross Geller, of Friends, do with his lottery winnings?

So what is a bond?

It is a type of fixed income investment known as a debt investment. When an investor purchases a bond, they are actually loaning their money to a specific entity, like the government, with the assurance that the loan will be paid back after a set period of time (on the maturity date), and over the time that the loan is maturing, the investor is paid a set interest rate. As a result, the bond holder receives a fixed income in compensation for loaning the entity money for operations.

There are two main benefits to bonds, and one important thing to keep in mind.

- Loaning money to an entity like a country is very low risk as countries are probably the most reliable debtors in the world (not many countries go bankrupt), and therefore, bonds can be a very low risk way of investing your money.

- Bonds generate fixed annual income, so you can have a reliable and predictable amount of cash flow from these investments, which are particularly useful for those who are retired.

The important thing to keep in mind is that bonds are purchased for a set value and produce a set return (yield). This return is constant for the life of the bond (eg. a 10-year bond), but the bond’s effective interest rate fluctuates with the value of the bond.

As a result, if interest rates on savings accounts go up, the relative value of that bond decreases because the money invested in the bond would have a higher yield in a different bond with a higher interest rate. Similarly, if interest rates go down, the value of that bond goes up because the interest rate on the older bonds are even more valuable in a low interest rate environment.

Example: A Canada Premium Bond is purchased for $10 and returns $0.20 annually ($0.20/$10 = 0.02 = 2% yield), while interest on savings accounts are 1%. If savings interest rates rise to 4%, demand for the bond will fall, and the value of the bond will decrease until it’s effective yield is greater than 4%, so less than $5 ($0.20/$5 = 4%).

The cumulative effect of this is that the value of bonds move inversely with interest rates. The higher the interest rate set by an entity (company, country, etc.), the lower the demand for older bonds set at lower interest rates. Therefore the value of that old bond is lower because your money can be better deployed elsewhere.

In Canada, another form of fixed income, low-risk investment, is a Guaranteed Investment Certificate (GIC). Similar to bonds, they are loans to the government for a set period of time, with the promise of repayment of the principal, with interest on the maturity date, which is set at 1 year or more.

GICs are very low risk (guaranteed to be paid back on investments up to $100,000), with even less volatility than bonds due to stable prices, and are also favourably taxed in Canada. They fall prey to the same problems as bonds, with diminishing returns (due to opportunity cost), if interest rates rise. The big difference, however, is that your capital is guaranteed to be preserved.

Example: $1,000 invested in a 5-year GIC at 3% is returned as $1,159.27 (3% annually, compounded annually over 5 years).

Fixed income can, and often should be a component of a stable investment portfolio due to their low risk. Of course, with lower risk, there is typically lower return. In the setting of market instability, however, it may be helpful to your portfolio’s overall health to have some of your investments in more stable investments.

A commonly stated rule is The Age Rule: your portfolio should hold fixed income in the same percentage as your age (eg. a 20-year old’s portfolio would hold 20% bonds/GICs and 80% other vehicles such as equities or funds). By no means is this rule hard and fast.

A Brief Aside: Diversification

Diversification is an investment strategy that involves spreading your dollars around among various, different investments. The theory behind this approach is that if you invest in multiple sectors, if one sector is performing poorly, the negative effects of that performance on your portfolio will be minimized by average or better returns in better performing sectors of the economy.

A general rule with diversification is that you must own at least twenty stocks to be adequately diversified in equities.

Example: You invest $10,000, putting $5,000 in Canadian banks, $3,000 in Canadian energy companies, and $2 000 in Canadian manufacturing companies.

The latest news causes a 10% drop in the value of your bank stocks. Meanwhile, energy companies surge 10% and manufacturing holds steady with no gain on the day.

Your portfolio is now $4,500 in banks, $3,300 in energy, and still $2,000 in manufacturing for a total of $9,800. This is a 2% drop, compared with a 10% drop if you had invested only in banks. Diversification has reduced your portfolio’s volatility.

Funds

Funds are a very popular, hands off way to invest. You can think of funds as a sort of team sport, where you work together with other investors. A financial company offers their services to manage the fund, which involves buying shares in companies on the stock market, or buying bonds. The money to purchase these shares or bonds comes from investors like you. A whole lot of investors like you. As a result, these financial companies are able to buy a whole lot of shares in a whole lot of companies, which creates… you guessed it…

DIVERSIFICATION.

You buy shares in the fund, where each share represents a fraction of all of the companies held in the fund. When companies in the fund do poorly, the value of the fund goes down, and when companies in the fund do well, the value of the fund goes up.

Meanwhile, the head honchos managing the fund charge a fee to manage the giant portfolio you have all bought into, with the intent that their management will make all of you a whole lot more money. The fee they charge is called a Management Expense Ratio (MER) and is expressed as a percentage. It represents the operating expenses of the fund as a percentage of the total value of the assets it is managing.

Example: The Great Canadian Mutual Fund (GCF) manages $100 million dollars in assets, and has an annual operating expense of $2,000,000 (Bay Street “geniuses” take a high salary and trading isn’t free). This makes the MER 2.0%.

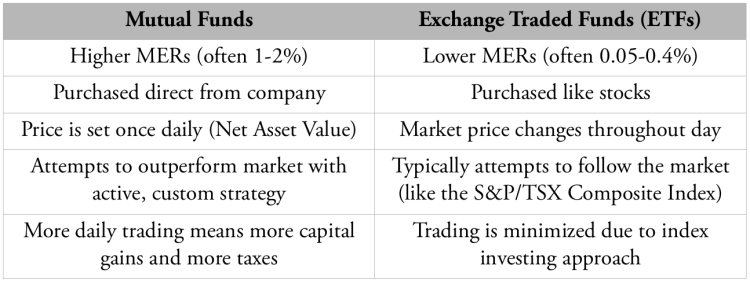

There are two kinds of funds that you can purchase, which I will compare and contrast below.

In either case, investing with funds is a more hands off experience, but this comes with a cost in the form of the MER.

The current trend in fund investing is shifting away from Mutual Funds to Exchange Traded Funds. This is due to ETF’s lower MER, as percentage point differences in expenses can make a big difference when they are COMPOUNDED over the life of the investment.

Additionally, research has suggested that despite the active management of mutual funds, the majority of them do not outperform the market as they advertise. In fact, a study by Standard & Poor’s has indicated that over a 5 year period, only 22% of Canadian equity-based mutual funds, and only 12% of American equity-based mutual funds actually outperformed the market in which they exist. This is in contrast to ETF index funds which, by definition, usually perform on par with the market.

We will talk more about funds in Chapter 5.

Wow. That was a lot. But we made it. You now understand the fundamentals of the environment we invest in:

- We invest in the global stock market governed by supply and demand.

- Basically, we can invest in stocks/equities, fixed income, and funds, each having its own pros and cons.

Stay tuned next Friday for Chapter 3, where we will discuss an approach to deciding how to invest, and the mindset needed to feel comfortable putting your money into the market.

Happy living,

JRM

2 thoughts on “OtOoI Ch. 2: Fine, I’ll Invest. What Do I Need to Know?”