Last week we outlined how to get to know your investing self, and explored a basic philosophy to get through investing without losing all of your hair. We talked about investment horizon, approaching investing with a minimum of emotion, and the idea of being a business owner.

Today, we will talk about where to put your money when you decide it is time to start saving for retirement. This will be from a uniquely Canadian perspective, as we discuss the various accounts available only in Canada. Some principles, however, are universal.

Emergency Fund

An important thing to consider is what you need your money for. Obviously you need to save for your retirement. You want to do that, otherwise you wouldn’t be reading this book. But there are other things to save for:

- A downpayment on a home

- An engagement ring

- That 2015 Ford Mustang

- Etc.

The point is, there are things that you need to save for where you plan to use that money sooner than twenty-five years. Sooner, even, than the next five years! I’ll reiterate this again.

Any money that you will need in the next 5 years should NOT be in the stock market.

You don’t want that money to be at a five-year low when you need it.

But if it is at a five-year low, you can just delay getting a house, or buying the ring, or riding around town in that sick whip of yours. Right?

But what about things that can’t wait? A car accident? Rent and food when you lose your job? These are things we can’t predict will happen, and we need to be prepared for them. So the first thing I would recommend to you is this:

You need an emergency fund.

This fund should be equal to whatever your monthly salary is (because you’re clearly getting by on that), multiplied by at least three months, or longer if you wish to be more conservative. This money should be liquid (ideally cash), and therefore not in the stock market. Sure, that money is depreciating at the rate of inflation, but a 2% chunk out of your savings each year is better than the 15% (or 20%, or 50%, or 5%) chunk you would lose if you had to liquidate equities at an inopportune time.

Once your emergency fund is established, you can start saving for your retirement, and all those other things you want. So, the next question is, where to save? You have a few options.

Savings Account

Exactly what it sounds like. This is your run-of-the-mill savings account at your chosen bank. You won’t get much of a return (in fact, none, due to the effects of inflation), but your money is generally considered safe. Stick your emergency fund here.

Registered Retirement Savings Plan (RRSP)

A Registered Retirement Savings Plan is one of the best ways to save for retirement. From within an RRSP, you may hold cash, purchase bonds, GICs, funds, or equities. As a result, you can tailor your RRSP portfolio to your desired level of risk and investment philosophy/strategy.

You may have multiple RRSPs, but your contributions to the RRSP are dictated by the Canada Revenue Agency (CRA) based on your income. This is because registration of the RSP makes it a tax-preferred account (see end of this section). When you make contributions to an RRSP, you are reducing your effective income by the amount you have contributed. This is because you plan to withdraw the money from an RRSP as income in your retirement (at which point you would be taxed on it), and therefore it would be unfair to tax you on the money twice.

The reason that this is beneficial is because you may be able to make contributions to an RRSP that lowers your income into a lower tax bracket, thereby reducing the total amount of income tax you pay for that year. At the very least, you will lower your income such that you pay less tax (because you made less money).

Over the year, you will pay tax on each paycheque based on an estimate of your annual income. The end result of an RRSP contribution, however, is that at tax filing time, your annual income will be effectively lower. You will have overpaid on income tax and will therefore receive a nice tax return, which you can then invest!

Example: Calvin earns $97,000 per year as an electrical engineer. The CRA deducts taxes from each paycheque in the appropriate amount (Calvin’s income lands him in the third tax bracket, at 26%, which begins at $90,000, we will simplify to 25% for this example).

He pays 15% on his first $45,000, 20% on the amount between $45,000 and $90,000, and 25% on the amount over $90,000. As a result, he pays $6,750 + $9,000 + $1,750 = $17,500.

This year, Calvin contributes $7,000 to his RRSP, lowering his effective income to $90,000. As a result, he is not required to pay 25% on that $7,000, and receives a tax return of $1,750, which he happily invests.

Another benefit to RRSPs is that companies often offer RRSP contribution top-ups to their employees. For every dollar an employee contributes, the company will, up to a point, match the contribution. For example, they may match 20% of your contribution up to $2,000 per year. You could contribute $10,000, and they would contribute $2,000 on your behalf, for a total contribution of $12,000. A 20% annual return! If you have this opportunity, maximize on it!

A final important benefit to RRSPs is that up to $25,000 in the fund can be used, tax-free, to buy or build a home (Home Buyer’s Plan, or HBP), as long as you pay it back within fifteen years. This is a great way to save for a down payment as it is cutting down on your tax burden in your young, good earning years (effectively increasing the amount you can save).

However, there are a few important caveats to RRSPs:

- You must be on payroll (not just earning dividends) in order to allow RRSP contributions (the CRA will set your annual deduction limit). This may be a factor to consider for entrepreneurs and small business owners who choose to pay their salary via company dividends.

- You will eventually pay tax on the money withdrawn in your retirement. The key there is that you will only withdraw as much as you need, which is often less in retirement (no kids, mortgage paid down, etc.), and therefore you will be in a lower tax bracket. The income you earned in your prime is taxed at a lower bracket in retirement, with the added benefit of reducing your tax load in those prime years.

- The amount you can contribute each year is set by the CRA. Check with them to find out how much you are allowed to contribute, or you may over-contribute.

For other tax reasons, an RRSP can be converted into a Registered Retirement Income Fund (RRIF), which gives you more flexible access to your retirement savings. The CRA automatically converts all RRSPs to RRIFs when you turn 71, but you may convert earlier than this.

A final note; registered is essentially a reference to the wide recognition of an account’s tax preference by countries other than Canada.

For example, an RRSP earning money from American investments is not taxed by the United States, because of the account’s registered status under our free trade agreements. This makes RRSPs an excellent container for any investing you may do in American equities.

Another example of a registered account is a Registered Education Savings Plan (RESP) as discussed in the previous chapter.

As a general rule, if an account is referred to as “Registered,” it suggests some level of tax protection.

Tax-Free Savings Account

The Tax-Free Savings Account (TFSA) is the preferred retirement savings vehicle for Canadians. So what is it?

It is a savings account, much like an RRSP, in which you can stash cash, or buy bonds/GICs, funds, or equities. You may have multiple TFSAs with different institutions (for example, a cash TFSA and an investment TFSA), but you are limited by the total amount that you can contribute each year, which is set by the Canada Revenue Agency.

TFSAs were first introduced in 2009, and in the first four years, one could contribute $5,000 per year to their TFSA. In 2013, and 2014, (and again, now in 2016), the annual limit was $5,500, and in 2015, it was a glorious $10,000. This means that if you do not currently have a TFSA, and were 18 before 2009, you have room to contribute $46,500 into a TFSA.

So why is it the preferred vehicle for retirement savings?

Again, it is a tax-preferred account (it’s in the name) like an RRSP, but its tax treatment is different from RRSPs, in that it is the inverse. Money that you contribute to the TFSA has been taxed (in that you earned it and it will be taxed in that year), but after that money enters the TFSA, it will never be taxed again by the CRA.

Example: Calvin earns $97,000 per year as an electrical engineer. He has significant cash savings, and after reading these posts, decides to invest it all in a TFSA.

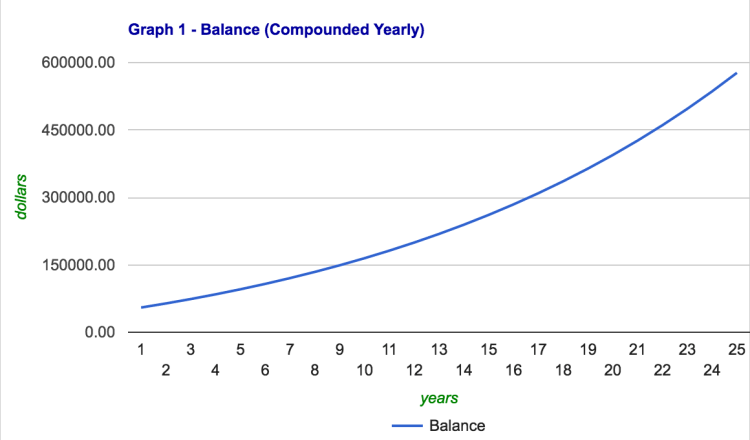

He invests $46,500 into an investment TFSA, maxing out his contribution room. He deploys the cash into various investment strategies (see Chapter 5) and manages a conservative 6% annual return over the next 25 years, adding the max ($5,500) each year to his TFSA.

When he retires after 25 years, he has contributed a whopping $184,000 of his after-tax income, but due to the power of time and compound interest, his TFSA portfolio is now worth over $511,000. He has made $327,000, tax-free, which he can draw on to fund his retirement, with no impact on his tax bill. He uses these funds to top up the income he is paid out of his RRSP.

This is how Calvin affords medical travel insurance for his frequent trips to Orlando, in his infirmity.

What this means is that you can withdraw from your TFSA to top up your income now, or in retirement (I recommend the latter), and you will not be taxed on it.

This tax preference makes it a perfect vehicle for long term investing because any interest that you earn over the years will be money you have made without a single penny being taxed.

A major benefit to the TFSA account is that it’s contents can be liquidated and withdrawn at any time for any reason.

The major drawback to this is that the withdrawn money cannot be re-deposited immediately, and instead, the amount withdrawn is added to the contribution room for the following year.

Example: Calvin withdraws $3,000 from his TFSA in 2015. Now he has to wait until 2016 to deposit that withdrawn money back into the TFSA, therefore, he deposits $8,500 ($5,500 + $3,000) in 2016.

Another thing to consider with TFSAs is that they are not recognized as Tax-Free in any jurisdiction other than Canada (note: it does not have “Registered” in the name). Therefore, any appreciation or dividends you receive from assets invested in non-Canadian companies may be subject to withholding taxes from the country of the company’s origin (for example, the United States).

A common misconception is that a TFSA is purely associated with a financial institution. A TFSA can, indeed, be opened at any respectable financial institution, but the amount that can be deposited is set by the Canada Revenue Agency. It is first and foremost, a tax shelter.

In other words, you can have as many TFSAs as you want, at as many different banks as you want, you are only limited by your contribution limit.

Cash Investing Account

Wow, you’ve maxed out your RRSP and TFSA contributions and you still have more to save? Good work!

Open up a cash investing account and start buying bonds/GICs, funds, and/or equities. Your money will still hopefully outperform inflation, but as this account is not tax-preferred you will receive an income statement from your financial institution at tax time, indicating how much you have earned, and how it contributes to your annual income (which will increase your tax bill).

You will take income on interest, capital gains*, and dividend payments**.

Conversely, you can also declare capital losses***, which work against your income and can actually lower your tax bill. Selling at a loss is not usually recommended, but in some cases, it may be beneficial (getting off of a sinking ship? Feeling that your portfolio is overweighted in a certain equity?). Consider carefully.

* Capital Gains: purchase a stock at $10 and sell it at $20, you have a $10 capital gain. Note, gains are only taxed when they are realized (meaning you need to sell that stock to be taxed on it, otherwise it is only a paper gain).

**Canadian dividends are taxed more favourably by the CRA than international dividends (it’s complicated, but comes down to the fact that dividends are paid from a company’s earnings, which for Canadian companies, have already been subjected to Canadian taxes, and therefore, should not be taxed fully twice).

***Capital Losses: purchase a stock at $20 and sell it at $10, you have a $10 capital loss.

Today, we talked about the various containers into which you can deposit your hard-earned savings and hopefully invest them for a comfortable (or extravagant) retirement.

We covered:

- The importance of an emergency fund.

- Basic savings accounts.

- Registered Retirement Savings Accounts

- Tax Free Savings Accounts

- Cash Investing Accounts

Our five-part series on investing for retirement concludes with Chapter 5 next Friday as we explore some of the various investing strategies and philosophies used.

Happy living,

JRM

One thought on “OtOoI Ch. 4: Where to Save”